HOME

/

INDUSTRIES

/

INDUSTRIALS

The industrial sector is undergoing a profound transformation fueled by automation, artificial intelligence (AI), and ongoing disruptions in global supply chains. As geopolitical tensions reshape trade dynamics and emerging technologies accelerate innovation, mergers and acquisitions (M&A) in industrial equipment, machinery, and aerospace & defense are creating substantial opportunities. To secure growth and resilience, companies are pursuing cross-border deals, joint ventures, and strategic investments that strengthen competitiveness, drive efficiency, and advance sustainability objectives.

At IMAP, we specialize in navigating the complex landscape of Industrial M&A. Our team provides expert guidance, industry-specific insights, and access to key strategic relationships that help clients make data-driven, confident investment decisions. Whether you're looking to sell your company, expand internationally, or restructure operations, our global partnership and market expertise ensure that you seize the right opportunities at the right time. We advise clients operating in:

The industrial sector remains a cornerstone of global M&A activity, recording over 18,000 completed transactions between 2019 and 2024 with a combined reported value exceeding €580 billion.

Industrial M&A continues to evolve amid shifting economic conditions, geopolitical uncertainty, and rapid technological change. Although deal volumes have fluctuated, investor appetite, particularly within the mid-market, remains strong.

Mid-sized transactions now dominate industrial M&A, reflecting investor focus on strategic growth opportunities and operational synergies that deliver faster value creation.

Higher interest rates and inflationary pressures contributed to a decline in total deal value, from €69B in 2023 to €57B in 2024. Geopolitical instability has introduced caution among investors, leading to slower deal flow compared to previous years.

2024 recorded 1,750 deals, marking a decline from 2,592 transactions in 2023 due to economic uncertainty.

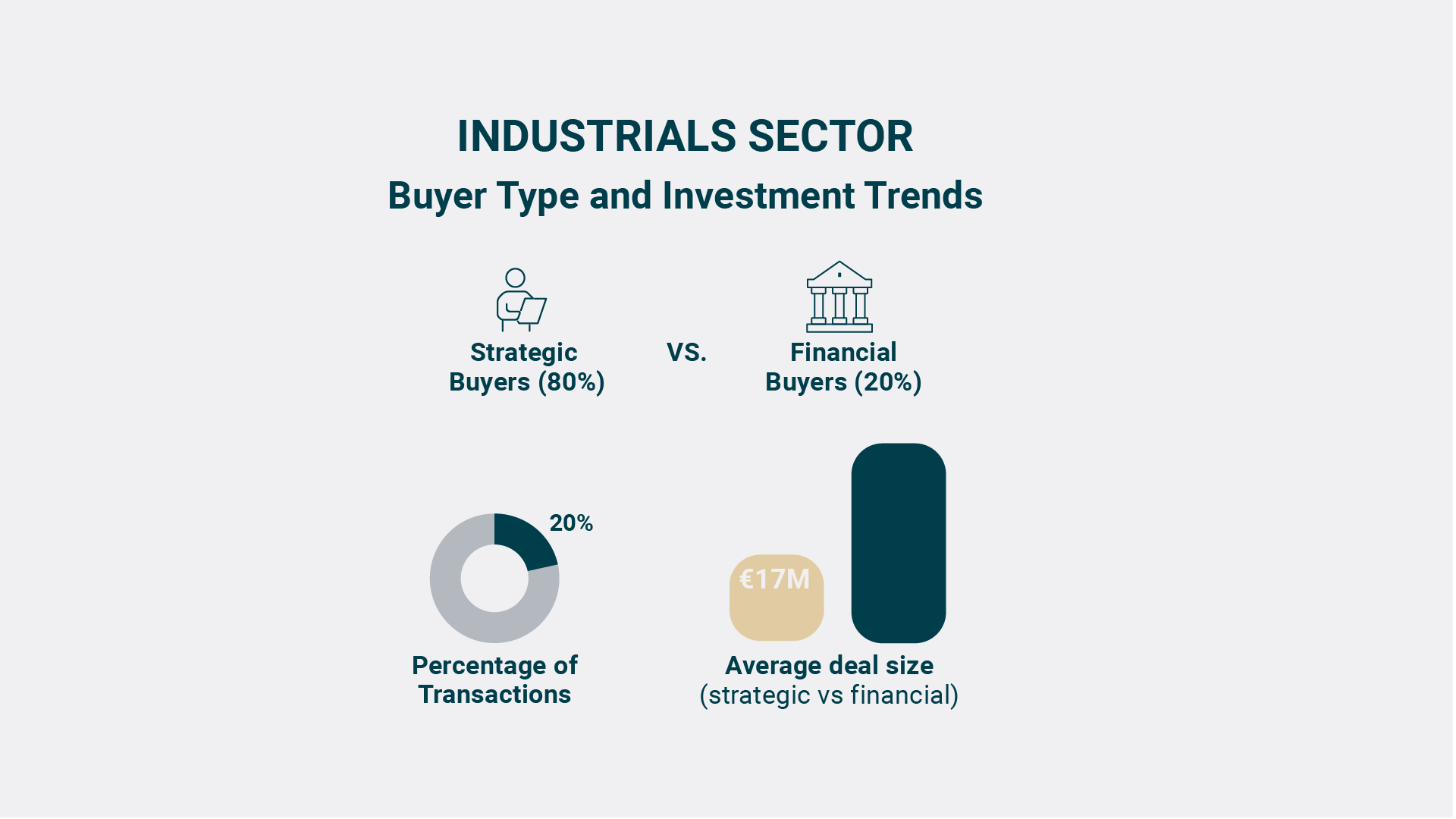

The median transaction value in 2024 was €17M, aligning with the trend of mid-market acquisitions.

85% of completed transactions involved majority stake acquisitions, while 15% were minority deals, asset purchases, or spinoffs.

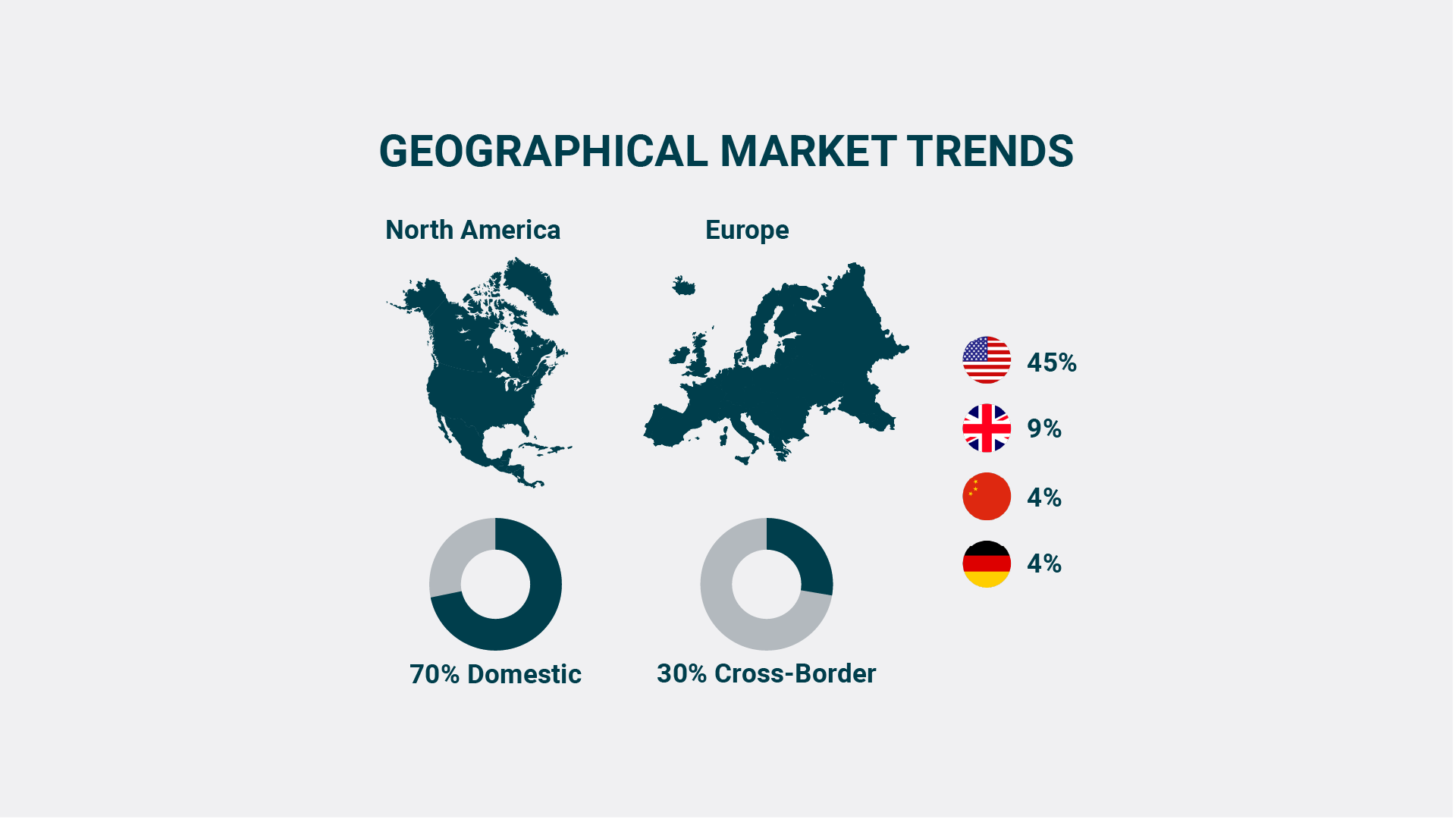

North America and Europe dominated M&A activity, contributing to 83% of total deal volume between 2019 and 2024.

The US (45%) led transaction volumes, followed by the UK (9%), China (4%), France (4%), and Germany (4%).

Cross-border transactions accounted for 30% of total activity, while 70% remained domestic.

Strategic buyers dominated the space, accounting for 80% of all transactions.

Financial buyers (20%) have maintained a steady presence, focusing on larger assets with an average deal size of €85M, compared to €17M for strategic buyers.

Private Equity (PE) activity remains robust, with 52% of European PE fundraising coming from the UK & Ireland in FY23.